The SmartCrowd Advantage

Finding the Best Property Investment Opportunities in Dubai

Dubai’s real estate market is known for its strong growth, making it a prime destination for investors worldwide. At SmartCrowd, our mission is to make

Dubai’s real estate market is known for its strong growth, making it a prime destination for investors worldwide. At SmartCrowd, our mission is to make

Dubai’s real estate market is known for its strong growth, making it a prime destination for investors worldwide. At SmartCrowd, our mission is to make real estate investment opportunities in

When we look at Dubai, we see the glittering lights, the towering skyscrapers, and the luxury lifestyle – but what about the numbers? If you’re looking to invest in Dubai

We’re proud to announce that we recently signed an MoU with RTA, marking an innovative step in the region to establish a blockchain-powered digital platform.

From affordable areas like Dubailand to luxurious hotspots like Zaabeel, find out where you should be investing in Dubai for the highest yields in 2024.

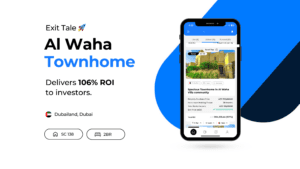

Explore our latest exit tale featuring our 25th success story in Al Waha, Dubailand. Find out how we delivered over 100% ROI in just three years!

Learn how to confidently make an investment in Dubai through fractional property investment so you can diversify your portfolio, and enjoy hassle-free returns.